Last Updated on March 11, 2026 7:39 am by Admin

This post is an ongoing work and this post will be split into separate posts as time allows. Therefore the information at this time is incomplete, but I think this information is important to share as soon as possible so this post is already public and may be found as I am editing it. I am currently awaiting more information to be provided per my paid public records request to the town, so keep checking back for updates.

Non-Profits, Impact Fees, and Municipal Services

No non-profit should be a burden upon the town in which it resides. Our current town administration operates under the misguided and wrong premise that non-profit entities are entirely exempt from paying for any municipal services at all. Non-profit organizations, while exempt from property and income taxes, still utilize municipal services like police, fire, ambulance services, sewer, roads, and schools. This usage can place a significant strain on local budgets, especially in towns where a large portion of the land is owned by tax-exempt entities, such as in Hardwick (33.43%!). This situation can lead to higher taxes for other residents and businesses or to reduced service levels, impacting the quality of life for all community members.

There is an argument for fairness in how all entities within a community should contribute to its upkeep. Non-profits benefit from these services just as much as for-profit entities do, yet they do not contribute financially in the same way. Voluntary “payments in lieu of taxes” (PILOTs) have been implemented in some areas, but these are often insufficient or inconsistent, leading to calls for a more systematic approach. Some argue that non-profits provide substantial community benefits that justify their tax exemptions. However, while these benefits are acknowledged, the direct financial support for public services like emergency response is seen as a separate issue. Non-profits might offset some costs through their community engagement, but this does not directly fund the operational costs of emergency services, which are critical for all residents including non-profit staff and clients. Therefore, a case can be made for non-profits to contribute financially to these services to ensure their sustainability and efficiency

Massachusetts law currently provides tax exemptions for non-profits under certain conditions to support their charitable purposes. However, there is an ongoing debate about amending these laws or policies to require contributions, perhaps through mandatory PILOT agreements or a new form of taxation tailored to non-profits. The discussion also includes the potential implications on the non-profits’ ability to serve their mission, but proponents argue that a small contribution might not significantly impact operations while greatly aiding public services

As a property owner in Hardwick, because of the irresponsible leadership of town government, you are burdened with the unannounced responsibility to pay for all of the town services for the non-profit entities within our town borders. On it’s face, this seems like a good thing. After all, non-profits are supposed to enrich and contribute to our overall economy and community making this a better place to live and raise a family. Well, that’s the way it is supposed to work.

Among the many non-profit organizations that operate within the Hardwick town borders, one stands out beyond all the others: Eagle Hill Foundation Of Massachusetts, commonly known as “Eagle Hill School”. They pay no property taxes and no impact fees. Instead, you pay. Click their logo below to visit their web site.

Eagle Hill School Campus and Employee Houses

Below is a satellite view of the Eagle Hill School Campus. It has grown tremendously over the years. It boasts a 62,000-square-foot athletic facility, a state-of-the-art cultural center, two year round fully licensed liquor bars, student housing, faculty housing, and the list goes on and on.

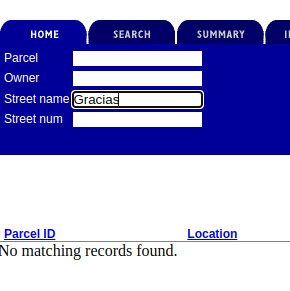

None of the houses on Gracias Way appear on the Assessor’s tax rolls. Click the image below and search for yourself:

The families that live in these houses and other faculty housing on campus can enjoy the amazing benefit of sending their children to Hardwick Elementary without the hassle of having to pay any property taxes. iGracias Hardwick!

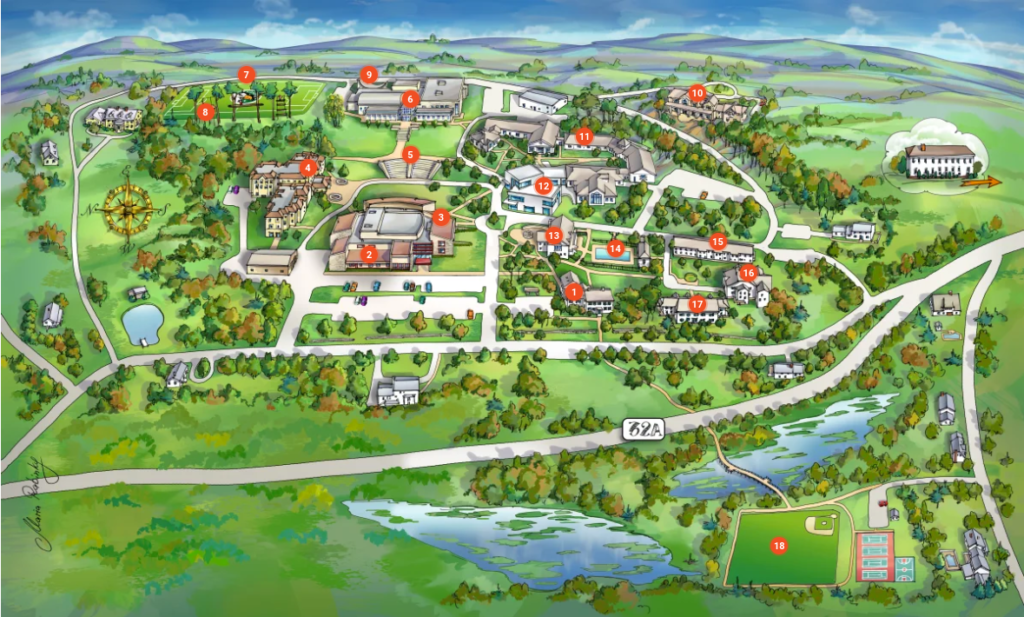

All of the land occupied by Eagle Hill School is still zoned for Agriculture (AR-60). Why was the zoning never changed? How were they allowed to build such large and elaborate buildings and facilities without making any zoning changes?

Below is the map from the Eagle Hill School web site. Notice all the buildings that do not have numbers? How many faculty houses are there? Where are the bars authorized by the liquor licenses?

Eagle Hill School Financials

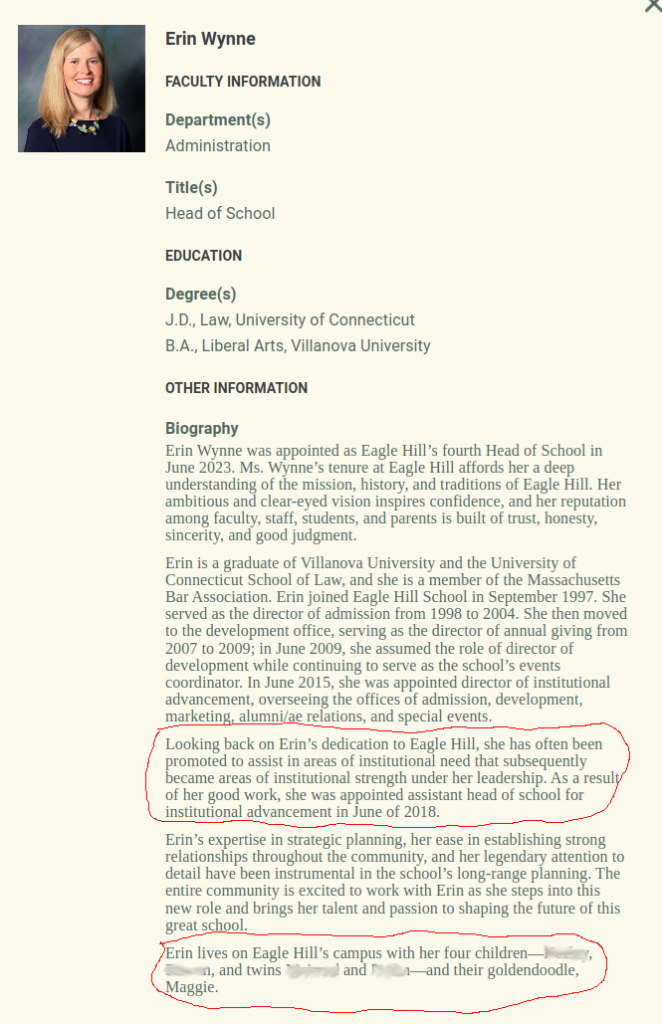

The new Head Of School, Ms. Erin Wynne, had the temerity to appear at the November 25, 2024 Hardwick MA Select Board Meeting and to claim that it is “financially not even possible for Eagle Hill “ to pay more for its “PILOT” agreement. (<– Click to view on YouTube)

Below is a summary of the financial information from IRS Forms 990 for Eagle Hill Foundation Of Massachusetts along side the “PILOT” payments (“gifts”) from Eagle Hill to the town. It is amazing how they have gone from $13 million to over $100 million in total assets in the past two plus decades.

I split this table in two to make it easier to see on mobile devices. Here are the numbers from the available IRS 990 forms from 2000 to 2022:

| Year | Revenue | Expenses | Net Income | Net Assets | Total Assets | Total Liabilities | Head Of School Salary |

|---|---|---|---|---|---|---|---|

| 2000 | $6,421,071 | $5,154,211 | $1,266,860 | $6,606,923 | $13,225,487 | $6,618,564 | $195,572 |

| 2001 | $5,152,448 | $4,841,582 | $310,866 | $7,038,730 | $10,219,289 | $3,180,559 | $187,155 |

| 2002 | $6,622,853 | $5,509,075 | $1,113,778 | $8,315,435 | $12,206,952 | $3,891,517 | $198,696 |

| 2003 | $6,788,469 | $5,858,324 | $930,145 | $9,537,613 | $19,768,695 | $10,231,082 | $204,265 |

| 2004 | $9,010,525 | $6,697,734 | $2,312,791 | $11,095,472 | $22,153,257 | $11,057,785 | $241,512 |

| 2005 | $9,779,041 | $7,870,619 | $1,908,422 | $13,075,363 | $24,214,510 | $11,139,147 | $274,001 |

| 2006 | $16,197,166 | $8,419,156 | $7,778,010 | $21,193,807 | $32,686,529 | $11,492,722 | $344,842 |

| 2007 | $15,780,013 | $8,809,843 | $6,970,170 | $26,999,481 | $43,973,713 | $16,974,232 | ??? |

| 2008 | $10,375,418 | $10,221,573 | $153,845 | $26,930,684 | $44,771,519 | $17,840,835 | $315,810 |

| 2009 | $13,291,634 | $11,364,680 | $1,926,954 | $29,316,357 | $44,832,983 | $15,516,626 | $328,844 |

| 2010 | $13,697,540 | $12,679,812 | $1,017,728 | $31,092,499 | $46,311,603 | $15,219,104 | $341,960 |

| 2011 | $16,216,345 | $13,111,377 | $3,104,968 | $33,752,685 | $50,432,485 | $16,679,800 | $470,022 |

| 2012 | $16,412,414 | $14,086,694 | $2,325,720 | $36,303,550 | $65,403,772 | $29,100,222 | $470,022 |

| 2013 | $19,095,900 | $15,891,798 | $3,204,102 | $39,767,359 | $69,137,381 | $29,370,022 | $466,149 |

| 2014 | $21,220,470 | $19,385,994 | $1,834,476 | $41,524,069 | $70,513,872 | $28,989,803 | $456,667 |

| 2015 | $20,422,879 | $18,349,901 | $2,072,978 | $43,560,315 | $72,115,164 | $28,554,849 | $512,064 |

| 2016 | $20,885,339 | $18,408,486 | $2,476,851 | $46,325,249 | $73,415,041 | $27,089,792 | $534,639 |

| 2017 | $24,064,610 | $18,717,654 | $5,346,956 | $51,678,334 | $78,174,675 | $26,496,341 | $701,053 |

| 2018 | $23,349,372 | $19,079,879 | $4,269,493 | $55,958,591 | $86,064,692 | $30,106,101 | $489,696 |

| 2019 | $23,024,967 | $19,024,176 | $4,000,791 | $59,893,815 | $87,454,244 | $27,560,429 | $486,769 |

| 2020 | $29,673,170 | $19,783,511 | $9,889,659 | $71,528,455 | $96,499,994 | $24,971,539 | $650,137 |

| 2021 | $24,485,162 | $21,136,187 | $3,348,975 | $71,300,636 | $95,855,505 | $24,554,869 | $600,244 |

| 2022 | $26,800,193 | $21,234,415 | $5,565,778 | $78,112,847 | $102,861,586 | $24,748,739 | $823,412 |

| 2023 | |||||||

| 2024 |

I added this table of the PILOT payments for visitors on mobile devices with smaller screens:

| Year | PILOT Payment | % of Revenue | % of Income | % of Assets | % of Head Of School Salary |

|---|---|---|---|---|---|

| 2000 – 2015 | Waiting for Public Records Request to be Fulfilled Apparently these records are difficult to retrieve. | ||||

| 2016 | $40,841.15 | 0.20% | 1.65% | 0.06% | 7.64% |

| 2017 | $46,737.60 | 0.19% | 0.87% | 0.06% | 6.67% |

| 2018 | $51,097.18 | 0.22% | 1.20% | 0.06% | 10.43% |

| 2019 | $53,156.56 | 0.23% | 1.33% | 0.06% | 10.92% |

| 2020 | $55,549.73 | 0.19% | 0.56% | 0.06% | 8.54% |

| 2021 | $61,661.61 | 0.25% | 1.84% | 0.06% | 10.27% |

| 2022 | $16,511.00 | 0.06% | 0.29% | 0.02% | 1.94% |

| 2023 | $53,297.00 | | | | |

| 2024 | $56,890.00 | | | | |

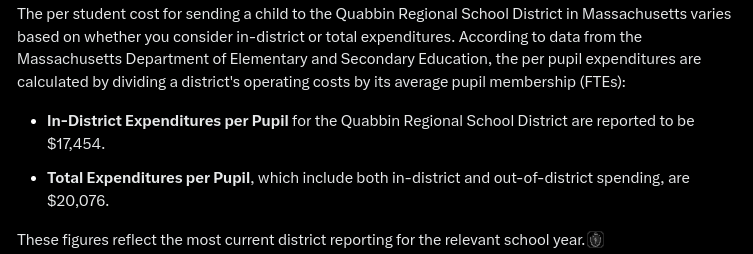

WOW! It would be hard to match that salary for the “Head of School” job in 2022 and I am still waiting for the 2023 & 2024 990 forms to see what it is now. What do you think of those PILOT payments? Considering that it costs the town around $20,000 per year per kid to attend Hardwick Elementary or Quabbin Regional, those payments don’t go very far at all.

I wonder how many of Ms. Wynne’s four children attend Hardwick Elementary or Quabbin Regional High School? What about those other faculty members living on campus? I know this is a little redundant from the numbers above, but here are the salary figures for “Head Of School” AND “Assistant Head Of School” since 2018:

| Year | Assistant Head Of School | Head Of School | Total | PILOT Payment |

|---|---|---|---|---|

| 2017 | $171,326 | $783,628 | $954,954 | $46,737.60 |

| 2018 | $175,588 | $489,696 | $665,284 | $51,097.18 |

| 2019 | $176,567 | $486,769 | $663,336 | $53,156.56 |

| 2020 | $188,466 | $650,137 | $838,603 | $55,549.73 |

| 2021 | $200,598 | $600,244 | $800,842 | $61,661.61 |

| 2022 | $259,258 | $823,412 | $1,082,670 | $16,511.00 |

Interested in the other “Highly Compensated Employees”? Have a look over here: https://www.sonsoflibertyma.com/2025/01/13/eagle-hill-school-highest-compensated-employees/

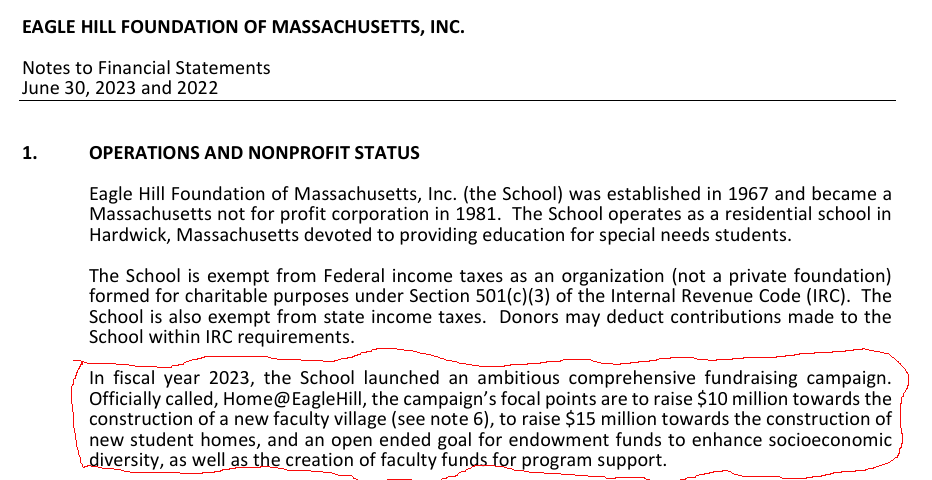

Below is the most recently filed financial statement for Eagle Hill School. In it you will find the word “Hardwick” occurs only one time, when referring to the school’s location. The word “PILOT” does not appear at all. It seems that if any payment or gift was made to the town, it was deemed insignificant enough to be part of a “miscellaneous” category and it is not specifically mentioned.

Not only does Eagle Hill School not acknowledge in any way the PILOT agreement with the town in their financial statements, they have “ambitious” plans to expand their property tax exempt housing for their faculty. The image below is taken from the financial statement document above:

As of spring 2025, EHS is living up to their plans and is aggressively expanding their faculty housing. The town government is allowing EHS to build whatever it wants, including brand new septic systems. No need to connect to that pesky sewer line they demanded the town build and maintain for them. No need for any site plans or impact studies. Just carte blanche do whatever they want…

If all of that isn’t enough, just hang on, there is more.

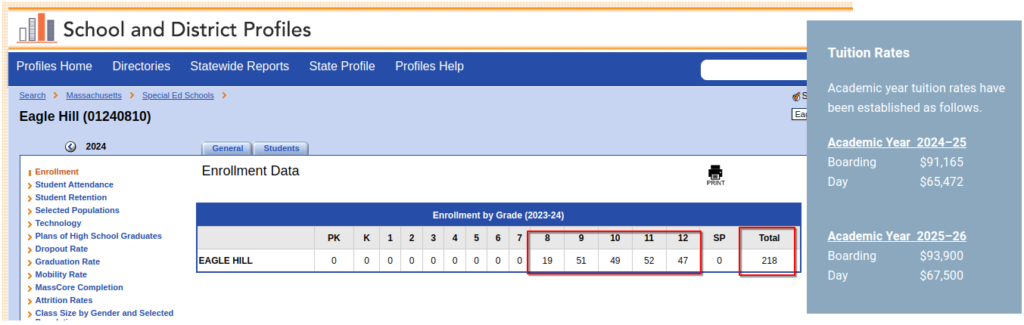

Checkout how much it costs to attend Eagle Hill School:

School Lunch Reimbursement

Why does such a wealthy school with such high tuition and fees need to apply to the state for lunch money? Also from the IRS Form 990, here are the amounts of money given to Eagle Hill School for Student Lunches from the state of Massachusetts tax payers along side the PILOT payments they generously gift to the town:

| Year | Massachusetts Department Of Education Bureau Of Nutrition For Reimbursement Of Meals Provided To Students | PILOT Payment |

|---|---|---|

| 2001 | $73,789 | |

| 2002 | $74,124 | |

| 2003 | $78,246 | |

| 2004 | $91,300 | |

| 2005 | $102,659 | |

| 2006 | $34,315 | |

| 2007 | ? | |

| 2008 | ? | |

| 2009 | ? | |

| 2010 | $135,403 | |

| 2011 | $142,975 | |

| 2012 | $169,674 | |

| 2013 | $165,323 | |

| 2014 | $166,680 | |

| 2015 | $171,812 | |

| 2016 | $170,251 | $40,841.15 |

| 2017 | $130,777 | $46,737.60 |

| 2018 | $173,154 | $51,097.18 |

| 2019 | $111,542 | $53,156.56 |

| 2020 | $147,787 | $55,549.73 |

| 2021 | $203,126 | $61,661.61 |

| 2022 | $153,508 | $16,511.00 |

It’s almost as if we tax payers paid Eagle Hill School more than Eagle Hill School paid us.

Calls for Police, Fire, and/or Emergency Medical Services

There are a staggering number of calls for Eagle Hill School every year. Although the majority are low priority (3) calls, there are hundreds per year. Each year there are also several high (1) and medium (2) priority calls. If Eagle Hill School is not the single biggest user of these services, they certainly have to be among the top users (which are also non-profit organizations, by the way). I am still working on this, I have the report for 2020 calls that I need to add here.

There are a lot of calls <– Link to source data

| Year | Call Priority | Number of Calls |

|---|---|---|

| 2021 | 1 | 21 |

| 2 | 5 | |

| 3 | 116 | |

| 2022 | 1 | 12 |

| 2 | 2 | |

| 3 | 139 | |

| 2023 | 1 | 19 |

| 2 | 7 | |

| 3 | 98 | |

| 2024* (through Oct 23) | 1 | 15 |

| 2 | 7 | |

| 3 | 134 | |

| Total Result | 575 |

There were 1,570 575* calls responded to at Eagle Hill from Jan 01, 2021 to Oct 23, 2024. How many calls did you have at your house last year?

There was a miscalculation in my spreadsheet for counting total calls by priority which has been corrected.

Here’s a table of the priority 1 calls for Eagle Hill School and the town. Oddly, the town reported a lower number for 2021 than I found in the call report.

| Year | 911 Calls (Priority 1) for Eagle Hill School | Total 911 Calls For Hardwick |

|---|---|---|

| 2020 | (*still working on this one*) | (Don’t have this number) |

| 2021 | 22 | 18(?) |

| 2022 | 14 | 112 |

| 2023 | 24 | 204 |

| 2024 | 17 | 175 |

Eagle Hill School “PILOT” Agreements

Notice how the PILOT payment amounts fluctuate? (see PILOT payments in the above table, in 2022 payments decreased) According to the agreement currently in place, reducing the payment amount is supposed to be done via a written request to be approved by the Select Board. I am currently waiting for a public records request to see if I can get more details about those reduced amounts, if/when they were requested, approved, etc.

Have a look at the current “PILOT” agreement that was finally put down on paper, voted on, and passed back on September 22, 2014. I haven’t found any evidence that it was reviewed by town council and it was probably not written by any Selectman (I wonder where it came from?). This agreement replaces a “verbal agreement” from 2005 that no one seems to know about except Vice Chair Vollheim. How was any of that ever legal? (Seems like the USDA didn’t think it was) The full agreement is below. It isn’t very long, have a look at the other provisions and ask yourself “Who benefits?“.

This is an additional recent PILOT agreement from June 24, 2024 regarding the sewer project specifically. This relates to the USDA document below.

The former town administrator “worked with” Eagle Hill School to create this agreement and it seems to be the only agreement with Eagle Hill School and the town that has been reviewed by the town’s lawyers so far. Also in that meeting the Select Board Vice Chair thanks Eagle Hill School for providing an emergency generator to the town fire department as well as decorative flags around town.

Original Recommendation for a “PILOT” Agreement

The Assessors office has maintained computations for what Eagle Hill School should be paying and it is quite surprising. Eagle Hill School consistently under pays for the PILOT agreement and they repeatedly breach the contract.

| PILOT Properties | |||

| Fiscal Year | Assessor’s Computation of PILOT Payment Rate | Actual Eagle Hill PILOT Payment | Difference |

| FY25 | $68,102.54 | ? | ? |

| FY24 | $65,357.72 | $56,890.00 | -$8,467.72 |

| FY23 | $56,209.79 | $53,297.00 | -$2,912.79 |

| FY22* | $62,150.13 | $16,511.00 | -$45,639.13 |

| FY21 | $63,037.98 | $61,661.61 | -$1,376.37 |

| FY20 | $61,534.19 | $55,549.73 | -$5,984.46 |

| FY19 | $59,153.92 | $53,156.56 | -$5,997.36 |

| FY18 | $56,998.03 | $51,097.18 | -$5,900.85 |

| FY17 | $52,320.00 | $46,737.60 | -$5,582.40 |

| FY16 | $46,258.14 | $40,841.15 | -$5,416.99 |

| FY15 | $44,130.45 | $0.00 | -$44,130.45 |

| FY14 | $42,163.46 | $0.00 | -$42,163.46 |

| Totals FY 14-24 | $609,313.80 | $435,741.83 | -$173,571.97 |

| * In FY22, Eagle Hill School unilaterally decided they would only pay the amount they computed, not the amount computed by the Town Assessor’s office AND they paid their top 2 employees alone over $1,000,000. From the town assessors office: The 2014 contract addressed only the taxable private residences which were purchased by EHS and therefore came off the tax rolls. When the 2014 contract was signed I interpreted the meaning of the contract for me, as an assessor, to create a PILOT based on the value of the properties and the current tax rate for each year. Therefore, I valued the properties just like every other taxpayer in Town :- current market value, value of any improvements or if demo or remodeling was done, those adjustments were made as was any other taxpayer. This was an acceptable interpretation of the contract until Fiscal Year 2022 when the new CFO at EHS challenged my numbers. He maintained that the value of the properties should not reflect any improvement. That is why the FY22 amount went down, he adjusted back “credits”. From that point on he has averaged our values and applied them accordingly across the properties. I still generate the PILOT on my own assessing procedures, but I believe that we receive a payment from EHS based on their interpretation of the contract | |||

If Eagle Hill School had paid the amount the Town Assessors office computed, they would have paid $173,571.97 more to the town from FY 14-24. If any of us tax payers just decided to pay less, we would certainly NOT get away with it.

Below are the so-called “Exempt” properties which are not included above. If these were not non-profit and they had to pay taxes like the rest of us, this is how much they would have paid:

| “Exempt” Properties | ||

| Fiscal Year | Assessed Rate (If not non-profit) | Tax Payment Due (If not non-profit) |

| FY25 | 1.32% | $924,396.35 |

| FY24 | 1.26% | $881,832.60 |

| FY23 | 1.33% | $877,354.05 |

| FY22* | 1.47% | $969,707.11 |

| FY21 | 1.57% | $887,426.83 |

| FY20 | 1.60% | $774,320.49 |

| FY19 | 1.60% | $740,507.45 |

| FY18 | 1.67% | $743,103.67 |

| FY17 | 1.60% | $710,254.40 |

| FY16 | 1.58% | $699,218.15 |

| FY15 | 1.59% | $641,242.23 |

| FY14 | 1.58% | $404,033.31 |

| Totals FY 14-24 | $8,329,000.27 | |

If we were able to collect this amount from Eagle Hill School, we could pay for a new fire truck with no problem. In fact, this would solve a lot of problems!! Also, remember that “Gracias Way” properties are not on the tax rolls at all. In fact, Eagle Hill School is currently building MORE housing.

The source data is in the “Original Data” tab of the spreadsheet below:

In 2005 the Board Of Selectmen wrote a letter to Eagle Hill School requesting a PILOT agreement:

And the current Headmaster of the School, P.J. McDonald rejected that offer:

USDA, Eagle Hill School, and the Town of Hardwick Sewer Commission

There is still a lot of research to do on this topic alone. It seems there is a lot more to the dealings over the “renovation” of the waste water treatment facility and the sewer line extension project that remains to be discovered. This could potentially become its own post in the future, but I am including this documentation as it is also relevant to Eagle Hill School.

Below is a document from the USDA that details some of the dealings between the town and Eagle Hill School (see page 6). Apparently there were problems discovered by the USDA that were supposed to be resolved before the project could be funded. It’s a lot to read, but really you can just skip forward to the changed parts they have helpfully put in red text. It is very interesting to see how they have scolded the town for the way they conduct business.

What is the loan debt the town owed to Eagle Hill School and why did they owe it?

What were the terms for the loan from Eagle Hill School?

Where is the written agreement that was required by June 18th by the USDA?

Resignation of Town Administrator Cofske

I noticed an old new story from 2021: https://www.masslive.com/news/2021/05/hardwick-town-administrator-theresa-cofske-quits-during-selectmens-meeting.html

During the April 26 meeting, she voiced myriad accusation against town officials, some of which are also included in her resignation letter.

Some of the division is related to a $17 million USDA grant that was awarded the town to upgrade the failing Gilbertville wastewater treatment plan, a project estimated to cost $27 million. The state committed $5 million to the sewer project.

There are no meeting minutes for the April 26, 2021 meeting and it was not recorded on YouTube.

So I requested a copy of the resignation letter. It is very interesting, see below:

Since the letter mentions a lot of stuff in email, I have requested the emails between Eagle Hill School and the Town for Jan 1, 2020 to June 24, 2021. It should be very interesting to see what was said.

Apparently there was a response filed by P.J. McDonald which can be viewed here:

Disposition Agreement in the Matter of Erik Fleming

On June 25, 2020, the Commission initiated, pursuant to G.L. c. 268B, § 4(a), a preliminary inquiry into possible violations of the conflict of interest law, G.L. c. 268A. On July 29, 2021, the Commission concluded its inquiry and found reasonable cause to believe that Fleming violated G.L. c. 268A, § 19. https://www.mass.gov/settlement/disposition-agreement-in-the-matter-of-erik-fleming

Remaining Questions

In the course of researching this topic, many questions are raised, keeping a list here for future research and updates:

- What other “gifts” to the town has Eagle Hill School made, such as the generator for the fire department and the decorative flags around town?

- Got the answer to this one. No monetary gifts were given. Only the generator and the flags besides the “PILOT” payments.

- In what ways, specifically, does Eagle Hill School contribute to the overall well being of Hardwick?

- Who wrote the September 22, 2014 PILOT agreement between the town and Eagle Hill School?

- How was the PILOT payment amount determined, what criteria was used?

- According to the Assessor’s Office, Eagle Hill School simply decides what they are willing to pay.

- Why does a school teaching grades 8 – 12 need

TWOa year round full bar liquor license (for 3 locations?)? - Why did the town have an outstanding debt and have to repay a loan to Eagle Hill School in conjunction with the sewer line project?

- Why does Eagle Hill School receive a reduced sewer rate?

- Why was the original PILOT agreement with Eagle Hill School not in writing and what exactly were the terms?

- So far I have been told that this was a “verbal agreement” between Eric W. Vollheim and the Head Of Eagle Hill School Peter J. McDonald. I am attempting to get more information. In the February 24, 2025 Select Board Meeting, Mr. Vollheim said EHS paid $25,000. Still not sure if there was more to the deal or if that is all, I have a paid public information request in pursuit of this answer now.

- Why is the land that Eagle Hill School resides upon zoned for Agriculture?

- How were they allowed to build such large and elaborate buildings and facilities without making any zoning changes?

- Which of the buildings on campus are not directly part of the non-profit mission?

- How many faculty houses are there and how many of their children are enrolled in our schools?

- Why are the houses for faculty at Eagle Hill School not on the tax rolls (Gracias Way)?

- Why isn’t Eagle Hill sent a bill for the hundreds of the Police, Fire, & EMS calls each year?

- Why has the Select Board shown favoritism and bias to Eagle Hill School rather than its citizens over the past decades?

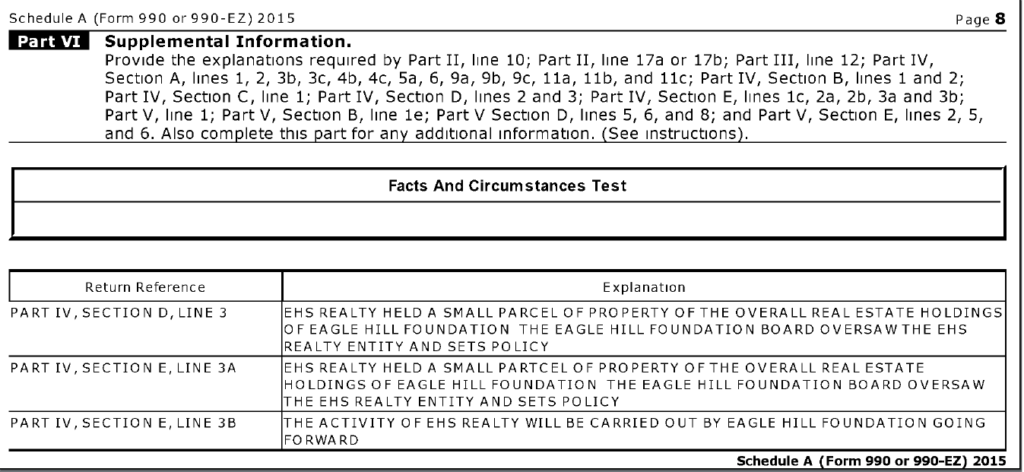

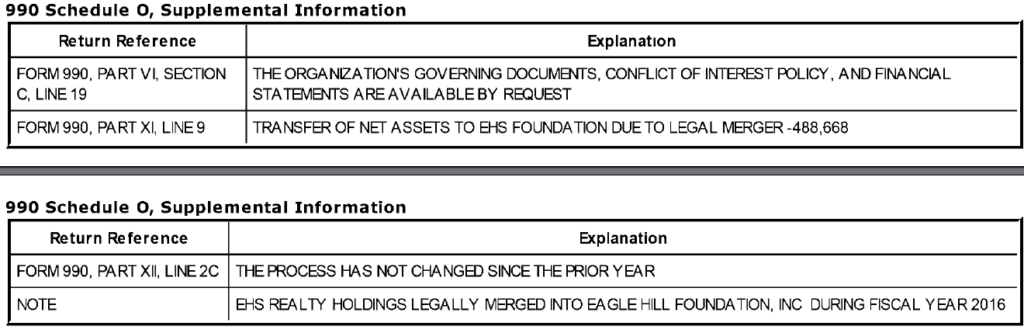

- What was “EHS Realty Holdings Inc”? IRS forms go all the way back to 2003.

Hardwick Select Board Members Over The Years

The “Select Board” is the key governing body in our town representing the executive branch of our local government. Ultimately, all decisions related to monetary issues (such as PILOT agreements, campus expansion, municipal service payments, etc.) are made by Select Board.

These are the members of the “Select Board” (or as it was known in the past, “Board of Selectmen“) over the years. I am working on filling out the details from public records, the items that are in italics are still being researched. Each member’s name is followed by the year in which their elected term expires.

| 2000 Gary Morissette (2001) Andrew Swistek (2002) Charles Lowell (2003) | 2001 Andrew Swistek (2002) Charles Lowell (2003) Eric W. Vollheim (2004) | 2002 Charles Lowell (2003) Eric Vollheim (2004) Andrew Swistek (2005) |

| 2003 Eric W. Vollheim (2004) Andrew Swistek (2005) Charles Lowell (2006) | 2004 Eric W. Vollheim (2004) Andrew Swistek (2005) Charles Lowell (2006) | 2005 Charles Lowell (2006) Eric W. Vollheim (2007) Deana Talbot (2008) |

| 2006 Eric W. Vollheim (2007) Deana Talbot (2008) Robert Roy (2009) | 2007 Deana Talbot (2008) Robert Roy (2009) Eric Vollheim (2010) | 2008 Robert Roy (2009) Eric W. Vollheim (2010) Richard Kmeic (2011) |

| 2009 Eric W. Vollheim (2010) Richard Kmeic (2011) Robert Roy (2012) | 2010 Richard Kmeic (2011) Robert Roy (2012) Eric W. Vollheim (2013) | 2011 Keenan Young (2012) Eric W. Vollheim (2013) Richard Kmeic (2014) |

| 2012 Eric W. Vollheim (2013) Richard Kmeic (2014) Keenan Young (2015) | 2013 Richard Kmeic (2014) Keenan Young (2015) Harry Comerford (2016) | 2014 Keenan Young (2015) Harry Comerford (2016) Richard Kmeic (2017) |

| 2015 Harry Comerford (2016) Richard Kmiec (2017) Keenan Young (2018) | 2016 Richard Kmiec (2017) Keenan Young (2018) Kelly G. Kemp (K. Allan) (2019) | 2017 Keenan Young (2018) Kelly G. Kemp (K. Allan) (2019) Julie Quink (2020) |

| 2018 Keenan Young (2021) Kelly G. Kemp (K. Allan) (2019) Julie Quink (2020) | 2019 Keenan Young (2021) Kelly G. Kemp (K. Allan) (2022) Julie Quink (2020) | 2020 Julie Quink (2023) Kelly G. Kemp (K. Allan) (2022) Keenan Young (2021) |

| 2021 Julie Quink (2023) H. Robert Ruggles (2024) Kelly G. Kemp (2022) | 2022 Kelly G. Kemp (2025) Julie Quink (2023) H. Robert Ruggles (2024) | 2023 Eric W. Vollheim (2026) H. Robert Ruggles (2024) Kelly G. Kemp (2025) |

| 2024 Kelly G. Kemp (2025) Eric W. Vollheim (2026) William F. Tinker (2027) | 2025 Eric W. Vollheim (2026) William F. Tinker (2027) Jeffrey Schaaf (2028) | 2026 William F. Tinker (2027) Jeffrey Schaaf (2028) _________________ (2029) |

Do you ever wonder why our town is broke? We don’t have enough money to maintain our fire hydrants. Our fire trucks are years past their expiration dates. We don’t have our own ambulance service anymore. We have to send our police over to New Braintree so they can have an office to work in. Our waste water treatment facilities are in terrible condition and instead of fully renovating, it is only a 50% renovation. We certainly do not pay our town employees enough and we are lucky to have them.

In 2024, Eagle Hill School “gifted” the town $56,890.00. It would take only 3 school aged children attending our schools at $20,000 each to completely use up that money. What if they had more than 20 children attending our schools? Why are the tax payers of Hardwick being asked to pay for a firetruck that will make hundreds of visits to Eagle Hill School each year and what is Eagle Hill School’s share of that cost?

There has been decades of the “good ole boy system” and “anarchy” where verbal agreements are made (just solve it with a phone call, right?), meeting agendas are vague, and meeting minutes are often not available or incomplete. Apparently following the law is considered optional. How could anyone ever even prove what happened?

I submit to you that Eagle Hill School is getting a free ride on our tax dollars. The poor should not be forced to subsidize the rich.

Contact your Select Board members and demand a better PILOT agreement policy in Hardwick with open and transparent negotiations. Demand that they establish impact fees that fairly recover the cost of municipal services used by non-profit entities.

Related Links: